- Total household wealth for December quarter rose 4.3%

- Residential assets were the largest contributor to this increase in household wealth

- Government and central bank stimulus primarily contributing to the rise

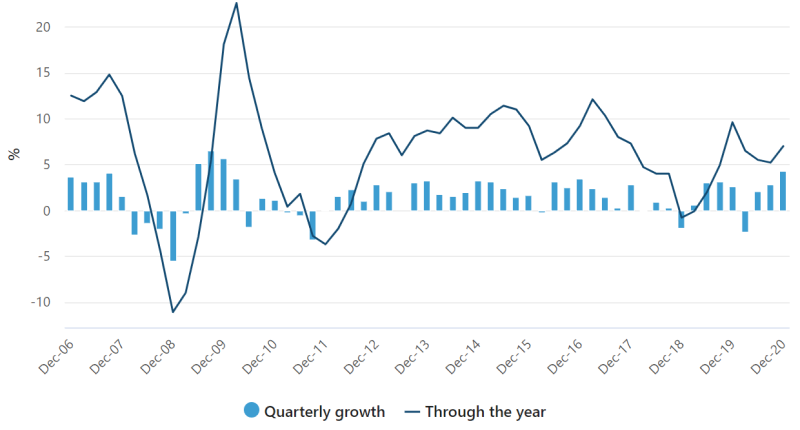

According to today’s data from the Australian Bureau of Statistics (ABS), total household wealth increased by 4.3% during the December quarter of 2020.

This is the largest quarterly growth since December 2009, which was the peak of the recovery from the Global Financial Crisis (GFC).

Total household wealth and wealth per capita were at record levels of $12,033.5 billion and $467,709 respectively. Over the year, growth was 7.0%, slightly below the long-term average of 7.3%.

Residential assets were the largest contributor at 2.1% of the overall 4.3% quarterly growth. They were also the largest contributor to the 7.0% throughout the year at 4.7%.

The ‘wealth effect’ – households spend more as the value of their assets rises due to feeling more financially secure – seems to be in strong play right now, with household liabilities increasing 1.0% ($24.2 billion) over the December quarter, with a $1.0 billion rise in short-term debt.

However, the housing debt to income ratio decreased 0.2% over the December quarter, as growth in income was greater than housing debt. This can be attributed to government income support packages, including JobKeeper and the Coronavirus supplement.

Household wealth drivers

As reported previously on The Property Tribune, government and central bank stimulus have played a major role in the rise of housing prices.

The Reserve Bank of Australia’s (RBA) expansionary monetary policies have reduced the cost of funding consumption and investment activities to historically low levels, encouraging lending to households and businesses.

This is reflected in the housing market with the growth of owner-occupier loans, which grew 1.9% over the December quarter (the strongest increase since December quarter 2016). Investor loans also rose 0.4%, marking the first quarter of positive growth since December 2018.

The cash rate target has remained at 0.1%, as well as the RBA conducting a $100 billion government bond purchase program (known as quantitative easing). This program is expected to be extended into the second half of 2021, indicating cheap money is here to stay longer than expected.

The latest reflection of the RBA’s influence is the interest rate price war going on between the big four banks, with three out of four passing interest rate cuts on their short-term fixed-rate home loans to their borrowers.

Furthermore, government policies such as the HomeBuilder grant and First Homebuyer Schemes have boosted housing market activity.

As auction clearance rates picked up since the September quarter, greater demand has outstripped the current supply of housing stock, driving the massive rises in property prices.