- Increases in real estate are not measured against CPI, excluding new dwellings

- Australia is currently experiencing its highest rate of inflation in 32 years

- Some early signs inflation is easing, although expected to remain high for rest of year

Although inflation has implications for housing demand, housing itself influences inflation, which can complicate the relationship between the two.

While increases in the value of real estate are not measured in the Consumer Price Index, new dwellings are, making it more complex.

Understanding the correlation between inflation and housing is important to make the market outlook for this year clearer, says a CoreLogic report.

Figures released by the ABS have found Australia is currently experiencing its highest rate of annual inflation in 32 years.

The Treasury and the Reserve Bank expect inflation to peak at over 7%. Households will respond by tightening their expenditure, with savings reduced and housing demand most likely remaining lower.

So, how does the housing market impact inflation?

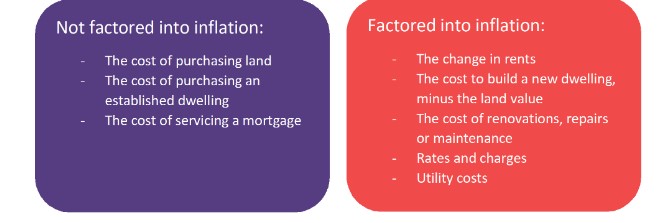

While inflation measures the change in the CPI – essentially a basket of typical goods and services consumed by households, governments and businesses – established dwellings are not included in this measure.

This is due to established dwellings being traded within the household sector. Land is not included as they are considered to be an asset, as opposed to a consumption good.

Mortgage interest costs have been excluded from the calculation of inflation since 1998, partly due to the RBA setting interest rates in the early 1990s to target inflation.

Continuing to measure interest costs made it difficult to understand the impact of monetary policy on costs in the economy.

Technically, the cost of owner-occupied new dwellings is included in inflation calculations, as are changes in rent values. Other costs associated with property such as rates, repairs, maintenance and renovations are factored in, too.

Around 23% of the CPI consist of housing components; 8.7% for new dwellings and 6.2% for rents, with the rest being other housing costs.

This all reflects the relatively large expenditure that households put towards housing costs.

“As a result, inflation is heavily influenced by changes in rents, new dwelling prices and utility costs,” said CoreLogic’s Eliza Owen.

“The annual change in the total housing component of the CPI was 9.0% in June 2022. This was the second-largest increase of the CPI components, behind a 13% surge in transport costs.”

Data from the Australian Bureau of Statistics from June 2022 quarter showed the annual increase in new dwelling costs for households was 20.3% (the highest in the series’ history). This is almost seven times higher than the series average of 3.9%.

Annual change in cost of new dwellings

Supply chain disruptions have constrained building material supplies, fuelling this rise. The value of rents in June also saw a 1.6% annual increase.

Inflation therefore impacts housing markets both directly and indirectly. Whether this is good or bad, it depends on what is driving the economy, along with other factors impacting the economy at the time.

Inflation can directly erode the value of debt, which is good for mortgages. As the economy heats up, wages may rise, but mortgage principles are fixed.

Wages, however, have not increased significantly. The ABS reported the wage price index was up 2.4% in the year to March, below the 3.1% series average growth.

In terms of the real value of housing, the most notable indirect impact of rising ifnaltion on the housing market has been increases in the cash rotes, notes Ms Owen.

“This is because the RBA aims to influence inflation using the cash rate setting. The RBA targets a measure of core inflation, which strips out short-term, volatile influences on the CPI. Annual, core inflation is currently tracking at 4.5%, well above the RBA target range of 2-3%.

“Given that core inflation is unusually high, and the unique ‘emergency low’ cash rate settings through the pandemic, the RBA is now lifting the cash rate at the fastest pace since the 1990s.”

How long will it take to tackle inflation?

Ms Owen said she expects inflation to remain high for the rest of the year given an array of domestic and international factors.

“Internationally, these include Russia’s invasion of Ukraine, the resurgence of COVID and COVID lockdowns in China, and capacity constraints in some segments of the economy,” she said.

“Domestically, extreme weather events have contributed to increases in some food items, and resilience in household spending remains an uncertainty.”

However, Ms Owen noted that there are early signs of relief in the market, such as a build-up in inventory in the United States, with commodity prices also starting to ease too.

“Money markets are indicating a lower peak in the cash rate than originally anticipated a few months ago, and CBA has suggested RBA cash rate cuts could be in store as early as next year. If these trends in easing inflation begin to manifest more widely, it could signal a floor for the housing market decline as early as 2023.”