- The cash rate rose much sooner than the RBA's initial forecast, lifted in March 2022 instead of 2024

- Housing values began to cool as a result, though the rate of decline is slowing down

- Housing accessibility no longer a focus, as the attention turns to serviceability of home loans

By now, Australians are used to riding the rollercoaster of the Australian property market.

Following a year of phenomenal price growth, 2022 was characterised by one of the fastest-tightening interest rates in history which saw prices cool accordingly.

As 2022 comes to a close, Corelogic has revealed the key property trends that have played out in the Australian market over the past 12 months.

Among these key trends are of course the driving force of rising interest rates, while inflation, worsening affordability, and lower consumer sentiment all receive a notable mention.

Expensive areas most vulnerable to interest rate rises

As a result, the national housing value fell by 3.2% in the year to November 2022. Additionally, the total estimated value of Australia’s housing market has declined by $2 billion since December 2021, reaching $9.4 trillion in November 2022.

All areas of the market were not uniformly impacted, however, with regional areas remaining more resilient than capital city areas.

Dwelling values in regional areas rose by 3.3% in the year to November, while capital city values declined by 5.2%.

Corelogic head of research Eliza Owen said the more expensive markets displayed sharper declines, as buyers in these areas often accumulate a higher debt.

Housing markets in the lower price end are more resistant to rising interest rates in comparison as buyers are not as financially extended.

Historically, homes in the upper quartile of dwelling values are significantly more sensitive to price fluctuations.

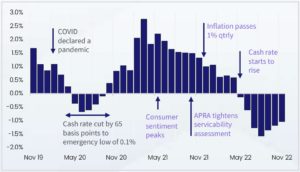

A year in the rearview mirror

The Australian market entered the new year with an air of confidence, off the back of a strong 2021.

Corelogic’s home value index indicated a rise of 3.0% between December 2021 and April 2022, though this represented a significant deceleration in the rate of growth compared to 2021.

Dwelling values officially began to decline in May however, when the RBA announced the first cash rate rise in over 11 years.

A decline in housing values intensified for four consecutive months before the rate of decline began slowing until the most recent figure in November.

Monthly change in national dwelling values

“The pace of decline has been slowing on a broad basis since September. While this may be seen as a positive by some, there is still risk of the decline re-accelerating in the year ahead,” said Ms Owen.

Since interest rates first began to rise in May, national dwelling values have fallen by 7.0%.

While it may seem that cooling prices are a positive sign for housing affordability, rising interest rates mean that serviceability could pose an issue for buyers and owners.

With more interest rate rises predicted for early next year, it’s likely the market could see the rate of decline in dwelling values pick up again.

“As we move into 2023, there continues to be a mix of headwinds and tailwinds for housing market performance.”

Eliza Owen, Corelogic head of research

“With expectations that the bulk of the rate tightening cycle occurred in 2022, housing value declines could find a floor in the new year. However, the extent of the floor in values could be further weighed down by mortgage serviceability risks, particularly for those rolling out of record-low fixed mortgage rates through the second half of year,” she concluded.